This post may contain affiliate links, which means I earn a small commission if you purchase something I recommend- at no additional cost to you! As an Amazon Associate I earn from qualifying purchases. Thank you for supporting this blog! Full disclosure here.

If you’re wondering how to save for an emergency fund, when to use it, and why you need one…keep reading!

We have been working hard to pay off all of our consumer debt for 3 years now! And it’s finally paying off, because we are just a few months away from becoming debt free.

Our next step is to save for an emergency fund, so of course we are diving in to learn everything we can as we create a plan for how much to save.

If you are ready to start your emergency fund savings too, I have some easy tips for you to follow.

Why do I need an emergency fund?

If you are living on a limited budget or income, you may be thinking, why do I need an emergency fund? It is hard enough to pay the bills each month! But that is exactly why you should focus on saving up for an emergency fund.

Life always finds a way to happen to us at the most inopportune moments, and if you are not properly prepared, you risk being in an even worse position than when you started!

Emergencies will happen, it is inevitable, so the best course of action is to try and create a safety net for yourself so that you do not go into debt every time something important comes up, something breaks down, or there is a medical emergency. Things that usually qualify as emergencies typically have to be dealt with very urgently, hence the emergency.

If you find yourself in a position without the means to really take care of that emergency, you will be totally unprepared and may have to go into further debt, especially for things that can happen suddenly, like medical emergencies.

If you’re still on the fence about needing one and are wondering how an emergency fund can benefit you, then keep on reading. In this post, I will take you through all of the steps from Dave Ramsey’s Baby Steps approach, which focuses on saving for an emergency fund and actually building up the fund for you and your family.

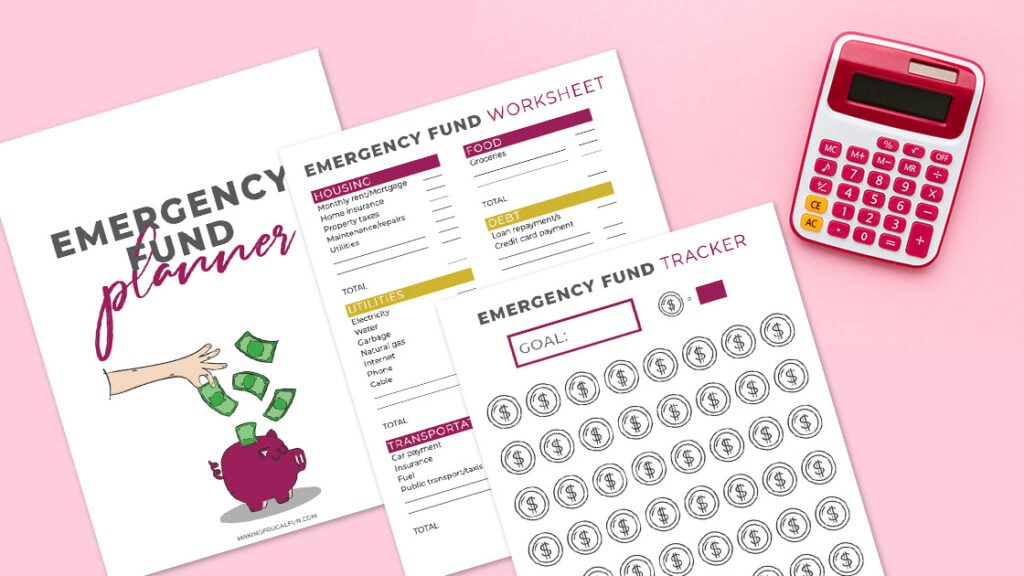

Grab this free printable emergency fund tracker by filling out the form below:

Emergency Fund Vs. Savings: What’s The Difference?

You may be saying to yourself, “Well, I already have a savings built, is that not the same thing?” And my answer to you is no! It is not the same thing. While some people may use these two interchangeably, they should be separate because they are for different situations.

The emergency fund vs. savings debate is one that occurs a lot in the world of frugal living, as many of us think that it is smarter to only keep one savings fund to be used for everything. I am here to tell you that that train of thought will lead to many empty savings funds and much anxiety over where the money is going.

A general savings fund should be used for long-term goals such as vacations, family planning, life purchases, an overall financial safety net, and general peace of mind and avoiding overdraft fees. On the other hand, emergency funds should be used in only specific circumstances, i.e., emergencies.

Situations that constitute the use of the emergency funds would be things like losing a job, hospital expenses that came up suddenly, a car breaking down, even things like flooding or heating and air systems needing to be replaced. Things like this are not usually planned for, which is why an emergency fund comes in handy! These are just a few emergency fund examples, but of course, there are many more, and you should try your best to be prepared for whatever life may throw your way.

This is why I started ascribing to Dave Ramsey’s baby steps program. If you want to read more about the full baby steps program, you should check out this post. However, in this post, I will focus on Step 1 and Step 3 of Dave Ramsey’s baby steps, which specifically help you start and bulk up your emergency plan funding.

How Much Should I Save for My Emergency Fund?

When you are just starting out on your baby steps journey, Step 1 details how to build up an emergency fund.

The starter emergency fund goal in this step is 1,000 dollars. Depending on your situation, this can seem like a lot, but if you stick to the baby steps about how to save for an emergency fund, you will be well on your way to that goal in no time. Now 1,000 dollars may seem like a lot but depending on the type of emergency and sometimes how crappy our luck can be, this can run out fairly fast!

This is why Dave Ramsey’s third baby step is to bump up your starter emergency fund to a bigger goal of 3 to 6 full months of expenses. This allows you to bulk up that 1,000-dollar emergency fund savings to an even heftier safety net for you and your family. It is also a very useful step because it is based on your monthly expenses, which means it can be individually tailored for your needs and is more achievable within your personal budgeting. Having an emergency fund that can cover up to 6 months of your expenses is a great way to give you and your family some peace of mind financially.

It also means that you should have a sizable balance in the case of nearly any emergency that should pop up unannounced for you. And instead of fighting a losing battle against keeping only 1,000 dollars in the emergency fund, you should be covered enough that even if you pull money out of it, you will not be starting back at zero. This will help to keep up the morale around creating and maintaining this special type of savings fund.

So, if you are starting out on this journey and find yourself asking, how much emergency savings should I have? My answer would be a starter fund of 1,000 dollars but don’t get too comfortable with just that! If you only keep 1,000 dollars in your emergency fund, it can easily be fully depleted by an extraneous car repair, which will tank your savings motivation and your account! Since we don’t want that, you will want to continue on through Dave Ramsey’s baby steps and eventually get to the third step, where you will bulk up that savings so that you can be prepared for anything.

Is 5000 enough for an emergency fund?

When it comes to a specific dollar amount for an emergency fund, it depends on your own individual financial situation. We discussed that a starter fund should consist of 1,000 dollars, but passed that you will want to evaluate your expenses and usual emergencies you have had come up in the past to try and assess the costs of probable risks that may occur in your life.

I suggest following Dave Ramsey’s specifications about a 3 to 6 months emergency fund, which is just an emergency fund that can fully cover your expenses for up to 6 months. In this way, you can tailor your savings for your personal emergency fund to a realistically achievable goal for your situation and your expenses.

Five thousand dollars may be plenty of money to a couple with a single child, but to a family of 6, it may seem a little sparse! So, while 5,000 dollars in emergency savings is a great goal for most people, you want to evaluate your own personal finances, emergency situations you have had to deal with in the past, and your monthly expenses.

If you cover yourself for up to 6 months of your expenses being paid, this will help you even if something like job loss takes a hit out of your income. As I said, you want to prepare for anything and everything the world may throw your way.

Where do I put my emergency fund money?

We have already covered the differences between an emergency fund and savings, but now you may wonder where is the best place for me to put my emergency fund? Well, there are a few different options, and they will all depend on your personal preferences and situations. I highly suggest not keeping an emergency fund in cash, I am a big proponent of using cash in many situations, but cash may not be the swiftest way to pay for things with an emergency fund.

Think about it, many places won’t accept large sums of cash as payment for things, and honestly, if you are shelling out a large sum of money, you should be getting a detailed receipt and proof from your bank statements so that you can assess more details later on if anything else happens. Also, suppose you have to pay a large sum of money for an emergency situation, and they do not accept cash. In that case, you are stuck waiting to deposit the cash, waiting for it to clear through your account, and even maybe waiting for the bank to open to deposit a sizeable amount of cash if you have an atm limit.

These are all things you do not want to worry about when an emergency comes around. These are all reasons why I suggest keeping your emergency funds in a bank account tied to your debit card. Now you may already have a savings account through your bank, but as we discussed, you do not want to mix the two together. Talk to your bank and ask about opening a specific saviFive thousandccount separate from your current one. This way, all of your funds can be in the same bank, just under different accounts.

In this case, a few other things to think about are, do you want to have the emergency fund under a joint account with someone, your partner, or possibly a parent? Or do you want to have an emergency account under your account only? This is a decision purely up to you and your level of financial trust in those around you.

I would suggest having at least one other trusted person that can access the emergency account. In this way, even if something happens to you, like a medical accident, or anything else that may incapacitate you in some way, there will be someone else you trust who can access those emergency funds to help you out of your situation.

How do I build an emergency fund?

Set your goal savings amount

The best first step for any financial decision is to set a goal for yourself! We have already gone over the common question of how much emergency savings should I have? While this number varies later on, if you are just starting out building an emergency fund from the ground up, the goal, according to Dave Ramsey’s baby steps, is to save 1,000 dollars. One thousand dollars is a fairly doable starting goal, especially if it is for cases of emergencies, which are usually expensive.

This number may seem scary at first, or maybe you already have saved this much, and you want to move on to the third baby step and save 3 to 6 months of your expenses into your emergency fund. Whatever path you are on, setting a clear goal for yourself will be what helps you power through and really bulk up that emergency fund.

Assign yourself contribution goals

Along with setting a total saving goal for yourself, you need to also implement contribution goals. This is because we all have been there, where we have set our total goal and then just think that it will be met naturally without any additional effort. We know that is just not the case, so setting up these contribution goals helps to keep you firmly on track to meet your total goal. While these should be firm contribution goals, they should not be unachievable.

That means if you know you do not have a lot of disposable income to divert away from your essential expenses, then you should give yourself more reasonable goals. If you live almost paycheck to paycheck, then giving yourself a contribution goal of 200 dollars a week is not feasible! That’s why you should take a look at your budget plan and current expenses and calculate how much money you have leftover every month or week that you may want to contribute to the goal.

Contributing on a regular schedule is much more important than contributing a lot of money whenever you can. There are also great ways to cut out some of the unnecessary expenses in your budget, opening up more room for savings. You can look here, for some great ideas about cutting out unneeded expenses on a low-income budget.

Once you have identified where you can cut out expenses and how much money you have leftover, you can account for a very achievable savings goal.

Start Small, then increase contributions

Similar to the tip above, if you are feeling overwhelmed at the prospect of saving a large sum of money for an emergency fund, then you should compartmentalize the savings journey! Don’t stress about getting to that final number, instead put a plan into place that helps you visualize the journey to that goal.

You can start with small contributions at first, and as you feel more comfortable or as you continue to cut unneeded expenses from your budget, you can increase your contributions. You don’t have to give yourself such strict rules that you are stressed out over your emergency fund building. That’s the opposite of what we are going for.

Your emergency fund building should be something that gives you peace of mind and a safety net for life’s mishaps, not something new to stress you out. So, take a breath and start small. Just like the baby steps for Dave Ramsey suggests, start with a small goal of 1,000 dollars, and then once you reach that goal, you can move on to really bulking up to that 3-to-6-month expense coverage amount.

Just remember, small contributions still make a difference, and once you feel like you can put in more money to the fund, you can readjust your goals. It doesn’t matter how fast you get to the goal, just as long as you keep looking ahead and actively participating.

Stay motivated

Staying motivated is one of the most important steps in any financial situation, but especially when it comes to savings and building up your accounts.

There are many ways to stay motivated, and one of the best ones is to set up a goal tracker! Goal trackers are amazing and so simple.

You may think that they don’t work, but I assure you they are a physical representation of your progress and will help you meet your goals. Each time you contribute to the emergency fund, you could mark off that amount or recalculate how much more money you need until you hit your goal.

Either way, having a way to watch your progress can make you feel like you are truly accomplishing something because you are!

Also, as we mentioned above, if you are feeling stressed out, it is okay to reevaluate your contribution goals and to ease up on yourself, don’t let that discourage you, and just keep pushing towards that goal even if you have to put in smaller amounts, that is okay.

Another way to help keep yourself on the path to your goal is to set up automatic transfers within your accounts. This takes out the guesswork of having to remember to actively put the money into the account and track your progress with the account through your banking app.

When Should I Use My Emergency Fund? Examples Of What It’s For

Medical Expenses

Medical expenses are definitely a qualifier for using your emergency funds. Medical emergencies are usually not planned and, unfortunately, very expensive, depending on your individual situation.

That’s why this is a good example of what your emergency fund is for, unexpected life events that can be quite costly and need to be covered rather quickly.

Home repairs

Whether you fall victim to a natural disaster, overuse of an appliance, or just regular wear and tear, home repairs can be expensive!

They are also something that usually needs to be fixed as soon as possible, like needing repairs to roofing, windows, heating, and air, or other appliances like the oven or washing machine.

These are perfect examples of things that require emergency funds.

Car repairs

We have all been there, you have a beaten-up old car that needs repairs sometime soon, but you don’t have the money. Alternatively, you could have been in an accident, and your insurance didn’t cover it, or it hasn’t cleared yet. These are all instances when you should utilize your emergency funds, especially if you only have one vehicle that you rely on one.

Job loss expense coverage

If you lose your job unexpectedly or have to move suddenly and know you will be without work for an extended period of time, this is a good reason to use the emergency funds. However, the funds should only be used to cover essential expenses during this time.

See also: How to Prepare for an Emergency when You’re Deeply in Debt.

Having An Emergency Fund Offers You Peace Of Mind You Didn’t Know You Needed

I hope this post has given you some good ideas for how to start saving an emergency fund, and a better idea of when you should use your savings for an emergency! Have questions? Leave them below!

hi! I'm shannon

I’m a wife, mom of three, doctor, and blogger! In 2018, I decided to turn my mom blog, into a personal finance blog so others could follow along on our journey to pay off over HALF a MILLION dollars in student loan and practice start up debt. I hope you enjoy following along, and maybe even find some inspiration along the way.